- Em que podemos lhe ajudar?

- 21 2240-0232

- 21 99624-5304

- [email protected]

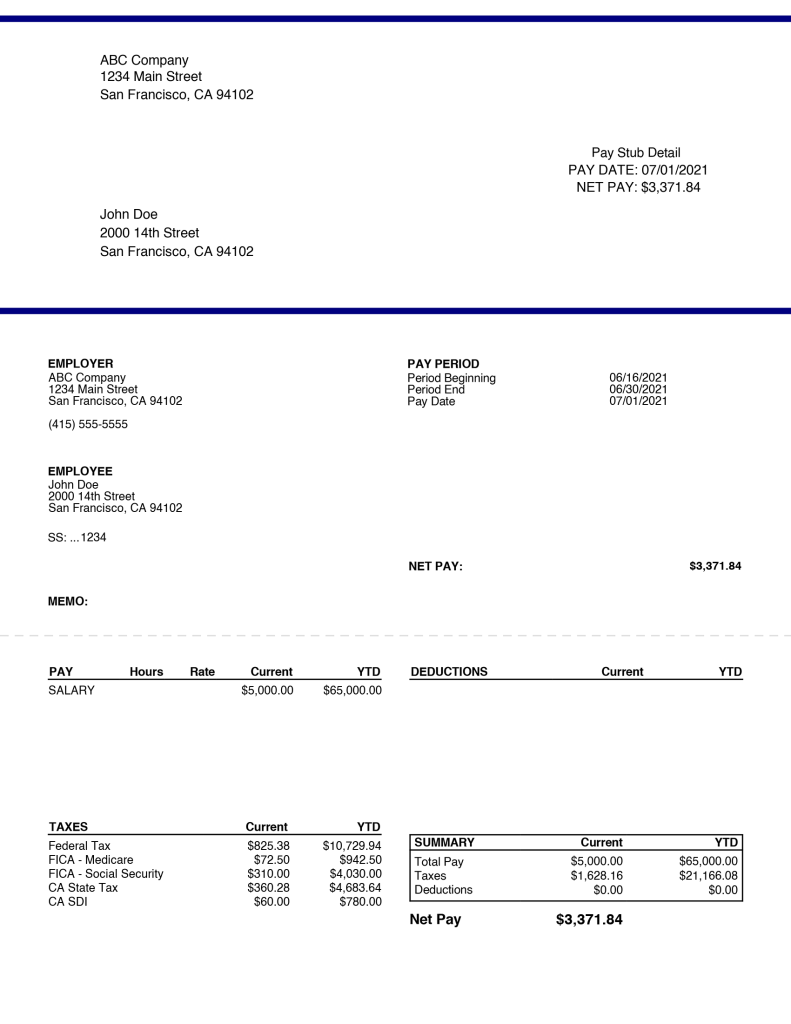

40-Year-Old Desires to Prevent Large-Expenses Employment: Should i Build 40,000 Monthly no Savings?

Online Kasino qua Taschentelefon bezahlen Telefonrechnung within Casinos?

Novembro 12, 2024Best Online casino Australia, Au Real money casino Genting casino Gambling enterprises 2024

Novembro 12, 202440-Year-Old Desires to Prevent Large-Expenses Employment: Should i Build 40,000 Monthly no Savings?

Refinancing your own financing to lessen interest levels or increasing your money as a consequence of front side hustles could help perform the debt weight

Ans: Provided your goals of becoming loans-totally free and you may retiring conveniently of the years fifty which have either a month-to-month income from 6 lakhs otherwise a corpus regarding 30 crores, it’s important to develop a strategic financial bundle.

First of all, let us address the financing. Which have a total outstanding mortgage out of forty-two lakhs and you can an effective car loan regarding 4 lakhs, your own monthly EMIs summarize in order to 140k. Your current month-to-month expenses is 142k, leaving little area getting coupons.

Given your own 7 lakhs regarding PF membership, using a fraction of they to reduce the highest-attention money will be useful. Although not, totally depleting your own PF might not be a good idea simply because of its impact on old-age offers.

Today, regarding the expenditures, if you are Tata AIA Luck Plus Plan can provide productivity, its essential to ensure that your insurance policies means are properly met alone. Avoid combo assets that have insurance policies to increase both factors.

To have old age considered, finding a monthly income regarding six lakhs during the many years 50 otherwise racking up a good corpus out of 30 crores necessitates a self-disciplined means. You may need to boost your capital contributions considerably and you can explore diverse money streams to reach like bold objectives.

Talking to an authorized Economic Coordinator offer personalized recommendations tailored with the financial predicament and you can desires. They’re able to assist framework an intensive economic package close financial obligation administration, capital tips, and later years believed.

Think about, reaching monetary liberty need hard work, persistence, and you will told decision-and then make. Stand purchased your targets, and with prudent economic government, you could understand your own aspirations.

Ans: Publishing Your retirement Earnings Means: An extensive Approach Their hands-on planning retirement which have a lump sum of Rs. 29 lakhs away from PF and Gratuity reveals foresight and you can relationship. Let’s framework a good investment package concerned about producing a monthly earnings of at least Rs. 20,000, making sure economic balances using your blog post-a career stage.

Information Your debts Well-done on your coming later years! Its commendable your taking strategies to secure debt future even after not having a retirement. Your own PF and Gratuity function a substantial foundation to own strengthening their old-age corpus.

Examining Income Means and you can Financing Vista Creating a monthly money out-of Rs. 20,000 need a proper-thought-out financing means designed with the economic specifications and chance threshold. Which have an effective around three-season financial support vista until old-age, prioritizing balance and you will uniform earnings generation is key.

Leveraging Logical Withdrawal Arrangements (SWP) Partnering SWP into the money package also have a reliable earnings weight article-old age. SWP enables you to systematically withdraw a fixed amount out of your shared funds financial investments at typical intervals, guaranteeing a reliable cash flow.

Ans: Hello; When you have an ongoing mortgage responsibility, never ever think of quitting established work unless you range-right up a new work possibility

Allocating Pension Corpus Fixed-income Devices: Allocate a critical portion of your corpus to help you fixed income products such as for instance Senior Discounts Scheme (SCSS), Post-office Month-to-month Earnings Program (POMIS), or repaired deposits (FDs) to include stability and typical money.

Loans Shared Fund: Imagine using a portion of your own corpus indebted mutual funds having SWP establishment. This type of loans offer possibility high productivity as compared to conventional fixed money devices while keeping a conservative risk profile.

Well-balanced Funds: Talk about healthy money offering a variety of guarantee and you will personal debt loans Eva AL financial investments. These finance give growth prospective and additionally typical earnings distributions, right for retired people looking to a balanced method.

Normal Keeping track of and Improvements Regularly remark the fresh new results of capital profile and make expected changes based on business requirements plus growing financial means. Rebalancing new collection sporadically guarantees they stays aimed with your later years money requires.

Completion Of the leveraging SWP next to an effective varied portfolio out-of fixed-income products, personal debt common financing, and healthy money, you can achieve your ultimate goal out of promoting a monthly money off Rs. 20,000 article-old-age. Prioritize balances, feel, and you can typical monitoring to be sure a gentle and economically secure old-age.